As we head into the holiday season, the health of the newly acquired COVID shopper is top of mind. With the pandemic driving shoppers online, the retention and significance of this newly acquired cohort has become an increasingly important question. Utilizing spend data, we analyzed the overall health of new cohorts over the past six months for some of the largest retailers. Here’s what we found.

Key Takeaways

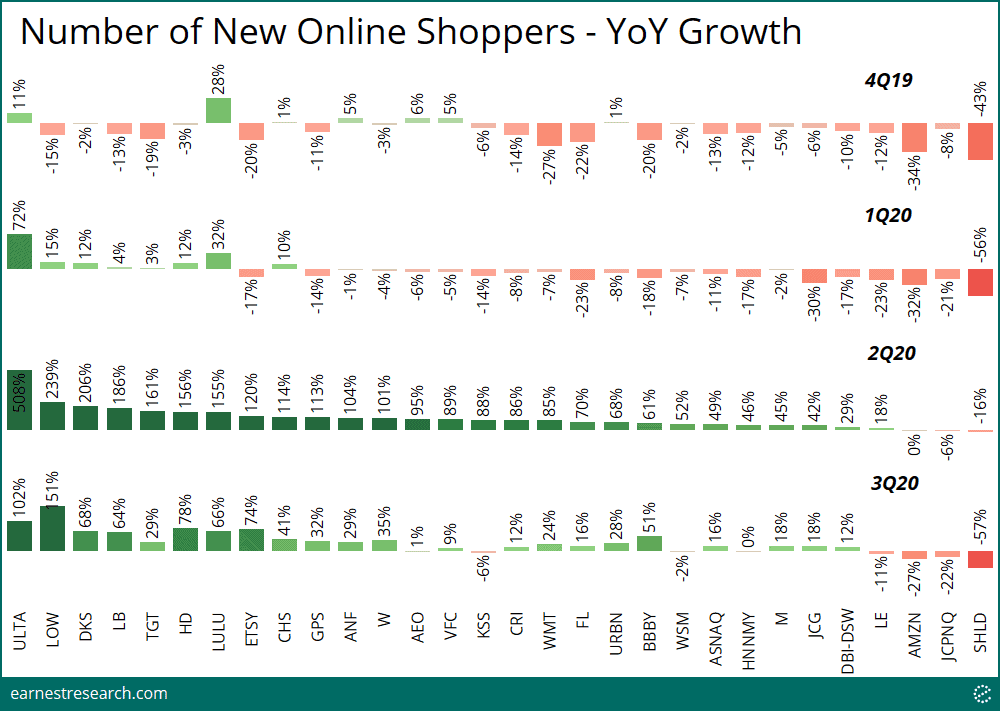

- While virtually all retailers saw a material spike in new shoppers online in 2Q20 due to the pandemic, some did at rates vastly higher than others. Ulta, Lowe’s, Dicks, Target, Home Depot, and Lululemon saw over 150% YoY growth of new online shoppers, while Sears, JCPenney, [Amazon, Lands’ End], and DSW saw growth of less than 30%. Ulta and Lululemon stand out as having acquired new online cohorts at a double digit pace consistently over the past year.

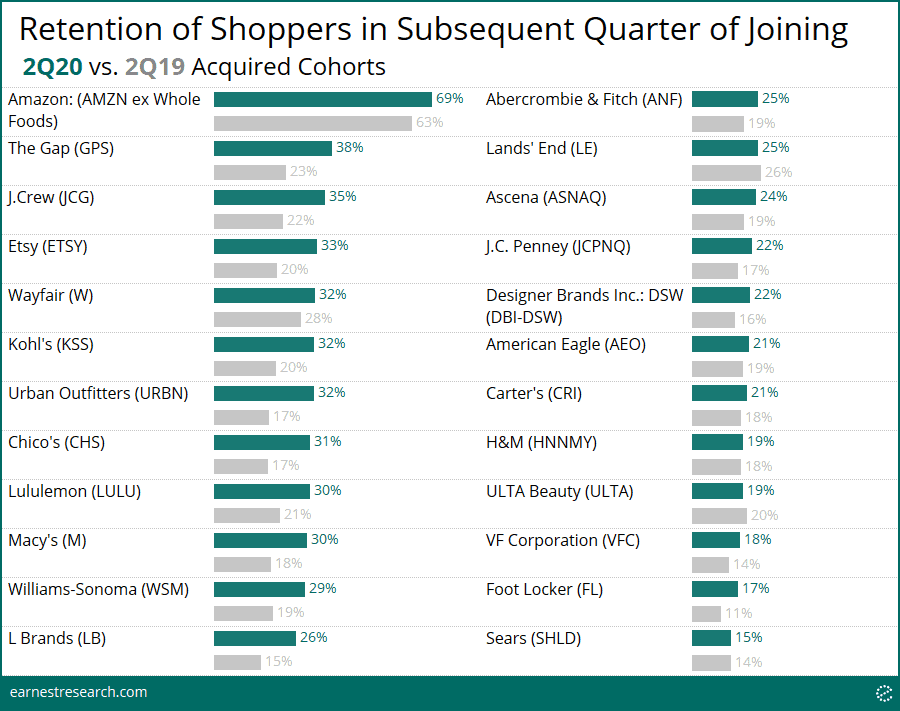

- More importantly, these cohorts have [so far] stuck around in 3Q20. Among virtually all retailers analyzed, the 2Q20 cohort saw higher retention rates relative to the 2Q19 cohort, with a sizable number of retailers improving their retention rates 10+ points, including Gap, J.Crew, Etsy, Kohl’s, Urban, Chico’s, Macy’s, William Sonoma, and L Brands.

- However, acquiring new shoppers (vs. retaining older existing shoppers) matters much more for some retailers over others. While Gap and Kohl’s, for example, saw high retention of their newly acquired ‘pandemic’ shoppers, the share that these new shoppers represent is relatively small. On the other hand, 30%+ retention for the newly acquired shoppers at Etsy, Wayfair, Chico’s, and Lululemon is much more meaningful, considering a sizable piece (15%+) of these retailers’ shopper base is typically new.

The New COVID Online Shopper

It’s no secret that there was a material spike in growth of new shoppers online in 2Q20 due to the pandemic. After all, it was the only way to purchase something in a brick-and-mortar-less retail environment. However, the uneven distribution of this online growth across retailers warrants a closer look.

Looking at the largest 30 retailers within broad retail categories, Ulta, Lowe’s, Dick’s, and L Brands saw the highest growth of new online shoppers in 2Q20, while Sears and JCPenney saw the least. (Amazon and Lands’ End, both effectively online-only retailers to begin with, would understandably not see many new online shoppers).

It is noteworthy though that many retailers with already mature online businesses saw material growth and continued growth into 3Q20 (J.Crew, Urban, William Sonoma, Lululemon, and Gap, for example, generated ~40%+ of sales online pre-COVID). Ulta and Lululemon stand out as having acquired new online cohorts at a double digit pace consistently over the past year.

But Are These Online Shoppers Sticky? Yes, They Are.

The big question is how sticky are these pandemic-driven acquired shoppers? To address this, we looked at the retention trends among the 2Q20 acquired cohorts, fully aware that this cohort was overwhelmingly—if not fully—acquired online. We compared their retention rates to the 2Q19 acquired cohort as a benchmark.

In all cases (except for Lands’ End, Ulta, and Sears), the 2Q20 cohort saw higher retention rates than the 2Q19 cohort. Additionally, a sizable number of retailers (9 out of 24 shown below) saw a 10+ point improvement in retention relative to last year: Gap, J.Crew, Etsy, Kohl’s, Urban, Chico’s, Macy’s, William Sonoma, and L Brands. It’s interesting to note that Ulta— despite substantially growing their online cohort this year—did not see improved retention relative to last year, remaining at [a healthy] ~20%.

How Much Do These New Cohorts Matter?

Retention of newly acquired shoppers is certainly important, but we wanted to understand how big—and therefore how crucial—acquiring new shoppers is for the retailers above. We therefore broke out the share of new vs. existing shoppers by retailer, and analyzed how this share trended over the past four quarters.

Wayfair, VF Corp, Lululemon, Abercrombie, Lands’ End, Chico’s, and Etsy, enjoy the highest share of newly acquired shoppers, accounting for ~15% to 40% of total. More mature retailers Amazon, Gap, Kohl’s, Macy’s, Sears, and JCPenney saw their share amount to ~6% or less. (Amazon’s share is understandably negligible as virtually all panelists have frequented the online giant by now).

Thus, despite Gap and Kohl’s, for example, seeing high retention of their newly acquired shoppers, the share that these new shoppers make up is small. On the other hand, 30%+ retention for Etsy, Wayfair, Chico’s, and Lululemon appears to be much more meaningful, considering a sizable piece (15%+) of their shopper base continues to be new.

Notes

Analysis done at the parent merchant level.